Chapter 7: Early Days of a Growing Trend: Nonprofit/For-Profit Academic Partnerships in Higher Education

Abstract

A chapter from Game Changers

Daniel Pianko and Josh Jarrett

Higher education presidents have lamented that the sector is caught in an "iron triangle," where access, quality outcomes, and costs are so tightly linked that institutions cannot improve one without negatively affecting the other two.1 However, enterprising college and university leaders are increasingly exploring a little-used strategy of nonprofit/for-profit academic partnerships to break this iron triangle. The best of these partnerships appear to be simultaneously expanding access, improving quality, and delivering financial sustainability. The worst of these partnerships trigger controversies with faculty, debate over mission alignment, bickering over resources, and unrealized benefits. Partnerships successfully break the iron triangle when each partner delivers specific value to a thoughtfully designed relationship with mission alignment and when carefully structured.

Does this herald a new era of collaboration and acceptance between the nonprofit and for-profit sectors, which have traditionally been at loggerheads, or is this a passing fad? This chapter argues that this is a trend that is here to stay and that we are in the early stage of rapid growth in these partnerships. We will provide a brief history of nonprofit/for-profit academic partnerships, explore the forces driving the growth in these partnerships, present lessons from successful partnerships, and asks questions for the future.

A Long, Quiet History of University Partnerships

The tradition of sharing best practices, learning, and resources is almost as old as the university itself. The first networks of universities have shared their library volumes—the heart of the research function—almost since their inception. Modern universities have increasingly outsourced core functional roles such as residence halls, food service, back-office processing, and academic-related areas such as book publishing or course design. As the market for education has become increasingly competitive, some universities have explored nonprofit/for-profit academic partnerships to bring needed capital and expertise to their institutions.

The modern nonprofit/for-profit partnership began in an unlikely place. One of the first such partnerships began in 1972, when Antioch College partnered with a for-profit group to create an adult-education center to reach African American students. That partnership eventually grew into what is now the nonprofit, historically black Sojourner-Douglass College. The Apollo Group, best known for the University of Phoenix, later started the Institute for Professional Development (IPD) to help nonprofit institutions build and manage their accelerated degree programs. However, some nonprofits viewed University of Phoenix as a threat or as a low-quality provider, and IPD's impact plateaued after some initial success. Nonprofit Regis University, a former IPD client, decided to build a nonprofit organization to provide such services at scale. Regis's New Ventures group grew quickly to over 10,000 students in only a few years. Together, Regis, Apollo Group, and a few other organizations represent the first generation of partner-led provision of core academic operations and functions to higher education institutions.

While the focus of this chapter is on nonprofit/for-profit partnerships, tax status is actually less relevant than provision of capital and skills. The Regis example proves that tax status is not a determinant of success or capability. One recent incarnation of a partnership structure—without the partner—is the University of Southern New Hampshire's online program, which has grown to over 7,000 students in just a few years through the separation of the capital and skill set required to build online to scale in a separate organization.2

Why Turn to Third Parties?

At their core and from the start, traditional colleges and universities are built to service 18- to 25-year-old students in a full-time residential setting. The traditional academic environment, ranging from summers off to baseball fields, is not designed to teach working adults whose jobs do not include breaks of more than three months or time for collegiate athletics. As nontraditional learners have driven the bulk of enrollment growth in higher education over the past two decades, attempts to support them have engendered nonprofit/for-profit academic partnerships.

Many institutions have discovered that moving outside their core expertise is extraordinarily difficult. Faculty, alumni, and other constituents sometimes object to perceived damage to the brand or to a potential adverse impact on their traditional operations. However, it has become clear that programs ranging from adult education to online learning require a radically different "product" to be successful.

Adults, for example, prefer an evening schedule and an andragogy-based approach to learning. The accelerated learning environment is typically located in a commercial real estate setting with instruction from practitioners rather than researchers. Nontraditional students generally consider their higher education options through direct marketing—a skill set unfamiliar to most admissions officers. From instruction by practitioners to the need for large call centers, few traditional institutions have the skills and personnel necessary to target this market.

Beyond the skill sets required and ambivalence from constituents, nontraditional learning environments require significant up-front capital investments and ongoing expenditures. Traditional institutions may have trouble allocating scarce capital resources toward renting new office space off-campus or spending the more than $1 million annually on advertising campaigns often necessary for reaching the nontraditional audience.

Partnership structures have evolved out of the long history of partnerships by and between colleges and universities. At times, universities have a specific need (e.g., how do we provide adequate remedial instruction?) or want to develop a new programmatic approach to further their mission. These partnerships can be divided into four primary areas (see Table 1).

Table 1. Examples of Partnership Structures

| Type | Description | Examples |

|---|---|---|

| Support | Outsource a single function or process for a university |

|

| Contract—Replica | Third party re-creates an existing program in a new format (e.g., online) | USC/2tor (2tor developed and manages a replica of USC's MAT degree online) |

| Contract—New | Third-party vendor leverages a university program or brand to create a new program, generally in a new format |

|

| Joint Venture Model | College/university and third party create a joint venture to build a new program with expectation of creation of new institution |

|

Why the Renewed Focus on Partnerships?

There are approximately two hundred nonprofit/for-profit academic partnerships serving upwards of 400,000 students.3 Virtually all of these partnerships are the Contract—New or Contract—Replica relationships described in Table 1.

- Contract—New: IPD alone has more than twenty partnerships with other providers, including Deltak. Regis partnered with another twenty institutions combined.

- Contract—Replica: The largest provider is EmbanetCompass, with approximately fifty relationships. Bisk Education is likely the second largest, with more than ten relationships.

Virtually all these relationships are low profile, though some, such as Indiana Wesleyan, have over 10,000 students in their IPD partnership. Several recent high-profile partnerships—both successful and unsuccessful—suggest that this is a growing trend. These partnerships are not trivial, requiring the alignment of mission and financial expectations, the garnering of stakeholder buy-in, and the execution of complex legal and operating agreements. Powerful trends must be at work if they plan to continue expanding. Indeed, a combination of forces is simultaneously bringing nonprofit and for-profit institutions closer to each other.

Trends Bringing Nonprofits to the Table

Nonprofit institutions—both public and private—must constantly assess how well they are meeting their missions and what, if anything, they can do to increase their impact in the face of external constraints. Increasingly, nonprofits are willing to explore partnerships with for-profits to help them meet their objectives. There are several trends driving this willingness.

The first trend is the recognition that postsecondary students are increasingly "nontraditional" and need different delivery models to serve them well. Today, up to 75 percent of students currently attending college are "nontraditional" based on Department of Education definitions.4

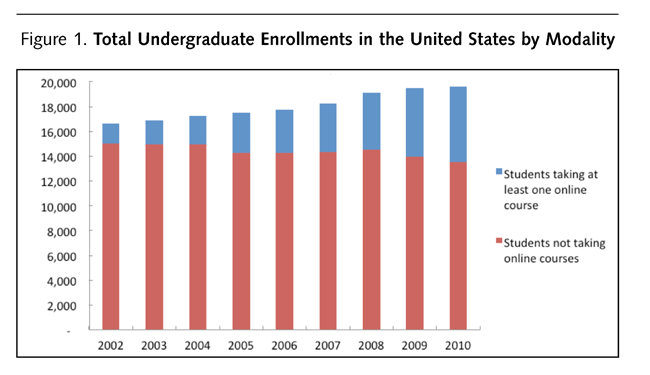

These students, initially older working adults but increasingly traditional-age students, are now flocking to online learning environments for their flexibility, convenience, and cost. A recent U.S. Department of Education meta-study cited evidence that online learning is as good as or better than traditional, in-person higher education.5 Today, over one in three college students takes at least one online course.6 See Figure 1.

The second trend is that accrediting bodies, state legislators, Congress, students, and parents are increasingly focused on measurable outcomes. The study Academically Adrift found that 45 percent of college students make no measurable progress on key skills in their first two years of college.7 There are few systems in place at traditional colleges to measure student outcomes, even when colleges institute compliant self-studies for their accrediting bodies. Due to the increased regulatory scrutiny of for-profit operators, however, such universities focus substantial resources measuring what they can measure—from employment outcomes to passing third-party exams (e.g., the National Council Licensure Examination for Registered Nurses, NCLEX). Across other disciplines, there are few nonprofit institutions that have scale, whereas for-profit operations have become extremely adept at quality control across multiple locations in complex service-delivery modules.

The third trend is declining resources and constrained capacity, driven largely by the great recession of 2008/2009 and continued fiscal pressures at the state level. Nearly half of the states have had spending cut more than 10% in the last year alone, and the cumulative impact of these reductions is severe. For example, current cuts in Arizona's state support for public universities, combined with previous cuts, reduces per-student funding 50% compared to pre-recession levels.8 Total revenues of U.S. higher education institutions declined 14 percent from 2007 to 2009, from $481 billion to $405 billion. During this same period, enrollment increased from 18.3 million to 20.4 million.9 This only compounded the problem. Tuition has risen 439 percent since 1982—almost twice the increase in health care and four times the rate of inflation.10 Students and their families are beginning to rebel against high costs, and universities can no longer expect tuition to cover a cost structure that is growing at such a dramatic rate.

Institutions simply have not been able to keep up with student demand with their existing funding models. A recent Pearson Foundation/Harris Interactive survey found that 32 percent of community college students were unable to enroll in one or more courses because they were full. This figure was 55 percent for Hispanics, 47 percent in California, and 45 percent among 20- to 21-year-olds.11 Worse yet, the California Community Colleges System was expecting to turn away up to 400,000 students from its institutions in the 2011–2012 academic year.12

The fourth and final trend is the absence of capital to finance growth and innovation. It cost the state of California almost $1 billion and took twenty years to build its latest campus, the University of California, Merced. Virtually no new medical schools have been built in the United States in the past twenty years because the average price tag for a medical school exceeds $100 million. In a time of severe budgetary constraints, it is virtually impossible to imagine statehouses allocating capital to expand capacity or programmatic reach.

At the same time, endowment returns and donations to nonprofit institutions have shrunk significantly in the great recession, with the bulk of funds raised at a limited number of elite institutions. Therefore, nonprofits that serve vast numbers of students will be forced to find expansion capital through other means.

Without their traditional sources of capital, universities will find it increasingly difficult to expand programs, add new sites, or grow online offerings without partnering with the private sector. Such partnerships are already happening in research areas and are rapidly expanding into programmatic areas.

Private sector capital appears willing and even eager to invest in education programs, assuming they can expect a reasonable return on their investment.

Trends Bringing For-Profits to the Table

For-profit investors, and perhaps the existing for-profits themselves, have their own incentives to pursue academic partnerships with nonprofits. Again, there are multiple factors driving this trend.

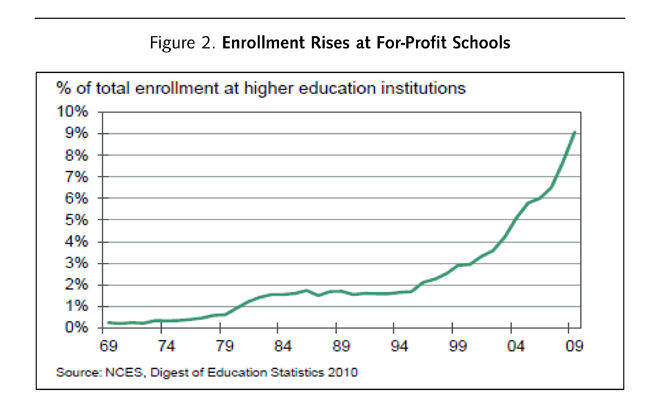

The first trend is that private-sector investors have experience in actively embracing the market serving nontraditional students—in particular, expanding the use of online learning and developing close employer partnerships. For-profits have experienced rapid growth, accounting for approximately 3 percent of the total market to approximately 9 percent from 1999 to 2009 (see Figure 2).

The second trend is the growing regulatory pressure on for-profits. The U.S. Department of Education has created a series of rules and regulations that primarily target for-profit institutions. These regulations require that the repayment rates of student loans among graduates must meet certain thresholds, and they also require that institutions seek regulatory approval for any new programs to be eligible for federal financial aid. (At the time of this writing, some of these regulations are under review.) These new regulations are on top of previously established rules, including a requirement that at least 10 percent of revenue must come from nongovernmental sources, as well as existing restrictions on competency-based awarding of credit for certain programs. Hybrid structures, in general, allow classification under the nonprofit rules.

The combination of growing regulatory pressure and increasing competition for new enrollment has seen year-over-year growth in new starts at for-profits decline sharply from +19% in 2009–2010 to –17% just a year later in 2010–2011.13

The third trend is the need to satisfy accrediting bodies. For much of the early 2000s, for-profits employed a strategy of converting a financially failing nonprofit college into a for-profit and recapitalizing the institution for rapid growth. However, several recent rejections of change of control have put the viability of that strategy into question. In 2010, the Higher Learning Commission denied Dana College's change of control, and other pending deals have dragged out for many months. As a result, for-profit institutions are increasingly looking to partner with nonprofits, as opposed to taking over and starting anew.

While it is still early in the widespread growth of hybrid structures, the accrediting bodies and Department of Education seem to be favorably inclined to approve—if not encourage—such operations. The key issue for accrediting institutions is that the entity that they accredit is the entity that retains academic control. So long as this key tenet remains in place, the accrediting body has limited authority to curtail the activity.

In addition, thousands of partnerships and relationships exist between institutions and vendors. These relationships can be deep-seated. It would be extremely difficult to define acceptable vs. unacceptable behavior. For example, how does an accrediting body draw the line between a college hiring a marketing firm and a call center operator but not a company that combines both? Instead, the accrediting bodies have stuck to their existing governance mechanisms to ensure the primacy of the accredited institution in all academic matters.

Putting Two and Two Together

So where does the value derive from putting nonprofit/for-profit academic partnerships together? There are two key answers: (1) specialization and (2) scale. Nonprofits have lower costs of student acquisition, more established brands, and deep faculty/academic expertise. For-profits have business-process expertise, experience with non-traditional students, access to investment capital, and scale economies. When the skills of each group are brought together, the combined offering can be stronger than either of the partners operating independently. This combination may be the difference between success and failure in an increasingly crowded and competitive marketplace.

Clay Christensen and the Center for American Progress have argued that higher education is undergoing a typical disruptive pattern.14 First, new technologies such as online learning enter the market. New entrants emerge and slowly gain scale before overtaking their more traditional counterparts. These new entrants create new business models that radically transform the operations of an organization.

At first, the new technology is inferior to traditional methods. For example, the first mobile phones weighed more than 15 pounds and were virtually useless but today's incarnations are an integral part of our lives and in many cases have replaced land-line phones. As new entrants become superior, most midsized players go out of business. Industries are shaped by a small number of large, dominant players that have access to capital and that continue technological innovation, while numerous niche organizations continue to provide some diversity.

Industries from cars to computers to department stores have undergone these dramatic transformations, as innovations in technology eventually lead to massive consolidation. Even in "services businesses," technology breeds a scale that was unthinkable before the disruptive innovation, e.g., there are now only four national banks, and nationwide names such as Wal-Mart and Target dominate the retail landscape.

Education may likely follow a similar path. University of Phoenix is the largest university in the United States. This scale has allowed for massive investment in the educational process. For example, Phoenix recently released a new cutting-edge learning m anagement system and acquired a leading computer-based math learning software.15 Currently, a University of Phoenix degree is generally regarded by many as low quality—the 15 pound cell phone—but it has been reported that Phoenix invests $200 million per year, or just 4 percent of its revenue, on improvements in its teaching and learning.16 This annual budget dwarfs the total spending of many individual colleges. The likely result is that over time, Phoenix will have the means to improve its quality on a scale the likes of which most institutions can only dream about.

So how can traditional institutions compete? Think of another analogy: how credit unions have successfully held market share relative to the national banks. Credit unions—virtually all nonprofits—have created partnerships with for-profit organizations in order to provide much-needed technology investment in strong, local brands. A credit union can use one company to process its credit cards while leveraging another service to provide online banking to its customers. Credit unions at this point can partner with for-profits to run virtually every part of their business. Virtually no credit unions attempt to match the capital investments of the big banks, but by working with a small number of for-profit providers, they have achieved scale necessary to compete effectively.

Key Partnership Design and Implementation Issues to Consider

Aligning key incentives between the partners is critical to the success of partnerships. Each partnership structure represents a unique set of issues to consider. Intellectual honesty for both the accredited institution and the for-profit organization is crucial. There are two key issues that tend to underlie successful contractual relationships:

- Financial: Virtually every partnership is driven by a mutual profit motive. The nonprofit envisions using the profits to create incremental resources to support traditional operations, while the for-profit will distribute profits to its investors.

- Mission: Colleges and universities are mission-driven and often seek to expand their reach, service, and impact. Working with a partner that identifies with the accredited institution's mission allows for a more constructive dialogue around the noneconomic issues that inevitably develop in a complex partnership.

A term sheet or a few sentences can define the economic relationship and mission alignment, but successful partnerships require deep thinking to drive through the myriad operational and legal complexities of such arrangements. To ensure a common understanding, the partnerships are structured through long, highly detailed legal contracts that lay out the specific roles and responsibilities of each party. Some of the key issues are as follows:

Accredited status: It is absolutely critical that the accredited institution retain the right to control all academic functions for any degree-granting program. This includes the ultimate approval rights over curriculum design, delivery, academic standards, and so forth. This control must be broad and absolute. However loath an institution is to pull the plug on a program, no accrediting body will accept a transaction whereby the governance of the degree-awarding authority does not continue to reside firmly with the accredited institution.

Key learning: The accredited institution must keep broadly worded control over any academic-program integrity issues. This responsibility must flow throughout the division of responsibility, with the accredited institution retaining specific control over a range of functions such as faculty, admissions requirements, and graduation standards. Best practice is to state the broad right of the accredited institution to oversee the program and then to point to specific standards that must be met. For example, all faculty must have certain types of degrees and the institution must approve all faculty hired, but the service partner can decide which faculty to hire and how much to pay them.

Specific direction for areas of control: Each contractual relationship should specify in specific detail the roles and responsibilities of each party. Documentation should break down the entire student life cycle into its component parts and then allocate responsibilities accordingly. Each party should be responsible for areas of its respective strengths or responsibilities—for example, the accredited institution would set admissions standards and review all applications, whereas the partner is responsible for all marketing and admissions activity.

Key learning: To the extent possible, the respective partners should set up definable rules for decision making ahead of time. For example, if the for-profit partner is responsible for admissions, then the accredited institution should define all admissions standards, including GPA, writing sample, official documents required, etc. It is virtually impossible to try to co-manage roles—and, in fact, generally better for the accredited institution to minimize involvement in decisions that are not core to its functionality. The accredited institution should consciously avoid input into as many tactical areas as possible because the needs of the new academic program will have myriad differences to their core operation. For example, many institutions have salary caps of some kind, but partners may be developing academic programs in areas whereby faculty are paid dramatically more than in a home institution (e.g., nursing faculty). By creating full separation between the institution's salary levels, the partner has the flexibility to hire faculty with specific skills at rates substantially above the levels at the home institution without creating issues at the next faculty senate meeting.

Performance management: Defining quality outcomes is difficult in any academic setting, but partnerships tend to optimize respective talents when each side agrees to the specific measurements of success. The objectives may be highly specific (e.g., pass-rate percentage on a licensing exam) or more qualitative (e.g., similar ratings in clinical placements).

Key learning: To the extent possible, performance metrics should be limited to key outcomes that drive the success of a program. It is difficult for a partnership to structure in advance program-development initiatives, but the partnership could define success as achieving a specific licensure from a specialized accrediting body, for example. If such specific licensure or related metrics are not available, others such as cohort default rate are broadly available and can be included as metrics of quality.

Financial considerations: There is a wide array of financial arrangements for partnerships, depending on the range of services provided by each party and the capital investment. While there are too many potential forms of economic consideration to list here, generally there is either a flat fee (or regulation-compliant per-student fee) or profits interest. The greatest alignment of interests generally comes from equity ownership, but allocating revenues can also allow each party to clearly define expenses related to revenue. In general, "revenue splits" would be something like 50/50 (50 percent to the marketing/financial partner and 50 percent to the accredited institution). For "equity" deals, the accredited institution will generally retain approximately 20 percent of the equity in joint venture agreements, although the market for such relationships is highly fluid, with few publicly available benchmarks.

Key learning: While there are numerous structures, there must be transparent reporting of financial information to all parties. Any partnership should have a third-party audit and frequent communication to ensure both sides understand respective revenues and costs. Long-term relationships work when both parties understand their respective economics, value the skills brought by each organization, and clearly define who gets what when.

Stakeholder involvement: Each institution has a complex web of stakeholders. It is imperative that the key decision makers on any partnership are fully aligned and have fully vetted the project. Generally this will include a board of trustees (or board committee) vote after careful consideration by key faculty and staff. One other note here is that many accrediting bodies know they need to evolve their understanding of such partnerships, but each accrediting body has slightly different rules, and these rules will evolve.

Key learning: Some of the most public failures of the partnership model occur when all stakeholders are not engaged. The most notable are those where the faculty vigorously protest a partnership based on quality concerns.

A View Forward—One Million Students Served Per Year by 2020

In this chapter, we have identified where nonprofit/for-profit academic partnerships have emerged, highlighted trends that are likely to accelerate development of these partnerships, and offered lessons learned to help future partners navigate their relationship. So where will this all lead?

Our back-of-the-envelope estimate is that 1 million students or more will be served by nonprofit/for-profit academic partnerships by 2020. As mentioned earlier, there are approximately 200 partnerships today serving nearly 400,000 students. Because of the trends previously described, we expect both the number and size of partnerships to grow. In recent years, these partnerships have been growing about 20% annually. Extrapolating that growth rate through 2020 would produce an estimate of 2,000,000 students enrolled in partnership programs. Using more-conservative estimates of 10% (the projected growth rate for online education) or 7% (the projected growth rate for the for-profit sector), by 2020 partnerships would reach approximately 900,000 students or 700,000 students, respectively.17 Despite the range of these estimates (a high of 2,000,000 and a low of 700,000), it is not unreasonable to believe that partnerships will serve 1,000,000 students or more by 2020. Assuming roughly 20 million total higher education enrollments, these partnerships would represent 5 percent of all enrollments.

The growth of nonprofit/for-profit partnerships will likely be steady but uneven over the next decade. There will be many quiet successes and a few public failures, à la the attempted Kaplan/California Community Colleges partnership, which was ended in the face of strong faculty resistance. It appears partnerships will find increasing acceptance among institutions, accreditors, policy makers, faculty, and students.

We will slowly develop a better understanding of what drives success. Many questions remain to be answered; this chapter simply begins the exploration of the issues in hopes that others will look at them more thoroughly over time. Undoubtedly, there will be many important lessons for all in higher education about how to potentially break the "iron triangle" of access, quality outcomes, and costs.

Notes

- John Immerwahr, Jean Johnson, and Paul Gasbarra, The Iron Triangle: College Presidents Talk about Costs, Access, and Quality (The National Center for Public Policy and Higher Education and Public Agenda, October 2008).

- Marc Parry, "Online Venture Energizes Vulnerable College," Chronicle of Higher Education, August 28, 2011.

- Based on forthcoming research from Innosight Institute, Harvard Business School, and The Parthenon Group.

- Paul Attewell, "The Other 75%: Government Policy & Mass Higher Education" (unpublished paper, 2008).

- Barbara Means, Yukie Toyama, Robert Murphy, Marianne Bakia, and Karla Jones, "Evaluation of Evidence-Based Practices in Online Learning: A Meta-Analysis and Review of Online Learning Studies" (U.S. Department of Education, September 2010).

- I. Elaine Allen and Jeff Seaman, "Going the Distance: Online Education in the United States, 2011" (Babson Survey Research Group, 2011).

- Richard Arum and Josipa Roksa, Academically Adrift: Limited Learning on College Campuses (Chicago: University of Chicago Press, 2011).

- See http://www.cbpp.org/cms/index.cfm?fa=view&id=3550.

- National Center for Education Statistics, Digest of Education Statistics 2010 (IPEDS) (46th in a series of publications, April 5, 2011).

- "Soaring College Tuitions," New York Times, December 3, 2008.

- Harris Interactive, Pearson Foundation Community College Student Survey (conducted September 27 through November 4, 2010).

- Nanette Asimov, "Community Colleges Could Turn Away 400,000," San Francisco Chronicle, March 31, 2012.

- JP Morgan analysis based on start growth at eight industry leading for-profit institutions.

- Clayton M. Christensen, Michael B. Horn, Louis Soares, and Louis Caldera, "Disrupting College: How Disruptive Innovation Can Deliver Quality and Affordability to Postsecondary Education" (Center for American Progress: February 8, 2011).

- Courtney Boyd Myers, "Clayton Christensen: Why Online Education Is Ready For Disruption Now" (blog post at http://thenextweb.com/insider/2011/11/13/clayton-christensen-why-online-education-is-ready-for-disruption-now/, November 13, 2011).

- Christensen et al., "Disrupting College."

- Based on forthcoming research from Innosight Institute, Harvard Business School, and The Parthenon Group. Future enrollment forecast from Eduventures.

Daniel Pianko is a partner at University Ventures Fund. By partnering with top-tier universities and colleges and then strategically directing private capital to develop programs of exceptional quality that address major economic and social needs, UV expects to set new standards for student outcomes and advance the development of the next generation of colleges and universities on a global scale. Josh Jarrett is Deputy Director for Postsecondary Success in the U.S. Program at the Bill & Melinda Gates Foundation. He leads the Next Generation Models portfolio, which supports learning innovations and technologies with the potential to dramatically increase low-income student success and improve affordability. Jarrett has previously served as an entrepreneur and as a consultant for McKinsey & Company and the National Park Service.

© 2012 Daniel Pianko and Josh Jarrett